Posted by Lawrence Gillum, CFA, Chief Fixed Income Strategist

Tuesday, May 23, 2023

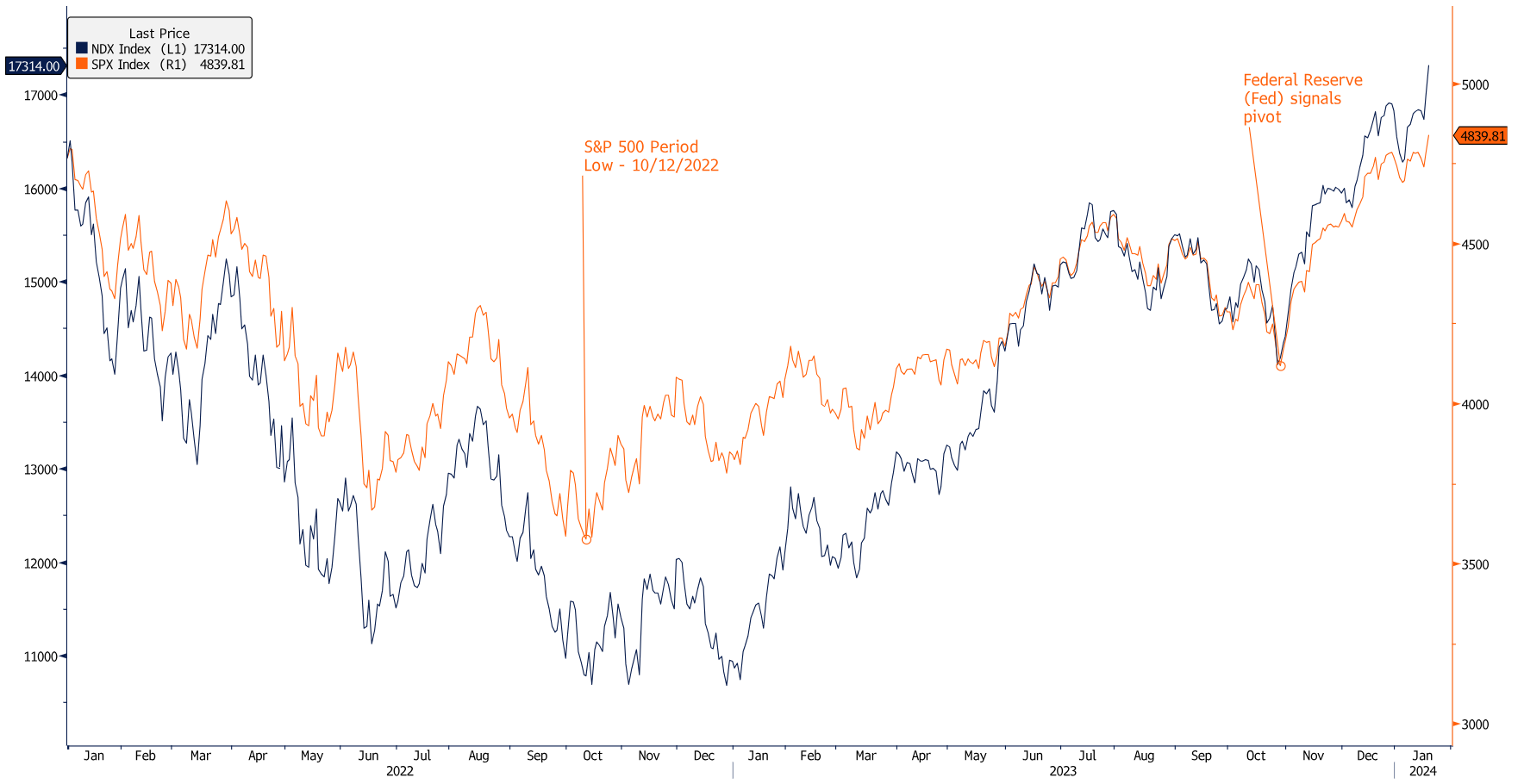

- U.S. Treasury yields are generally higher over the past week with the two-year trading around 4.4%. The 0.50% increase in the two-year yield since last Monday is largely due to markets pricing out rate cuts later this year. Our view was that the market was too optimistic for the amount of rate cuts being priced in. Markets now expect one cut this year, which may still be too optimistic, unless financial conditions deteriorate. That said, we think we’re close to the end of the recent rise in Treasury yields.

- News reports suggested there was “optimism” surrounding the debt ceiling negotiations but still no deal. Treasury market pricing suggests the greatest risk of delayed payment will occur for those securities that mature on or after June 6. Currently, the Treasury Department has around $60 billion in its operating cash account. For context, the Treasury’s cash balance got to around $11 billion in 2011. Our base case remains a deal gets done in time, but the clock is ticking.

- Moreover, the Treasury Bill (T-bill) market is fairly disjointed currently with T-bills that mature on May 30 yielding 2.89% (the fed funds rate is 5.25%) and those that mature in June 8 yielding 5.81%. The difference in yields between the two securities is at extreme levels as more market participants are avoiding those securities that could be negatively impacted by a delay payment from the Treasury. The longer the negotiations drag out, the more it is likely we’ll continue to see higher yields for the securities maturing in June.

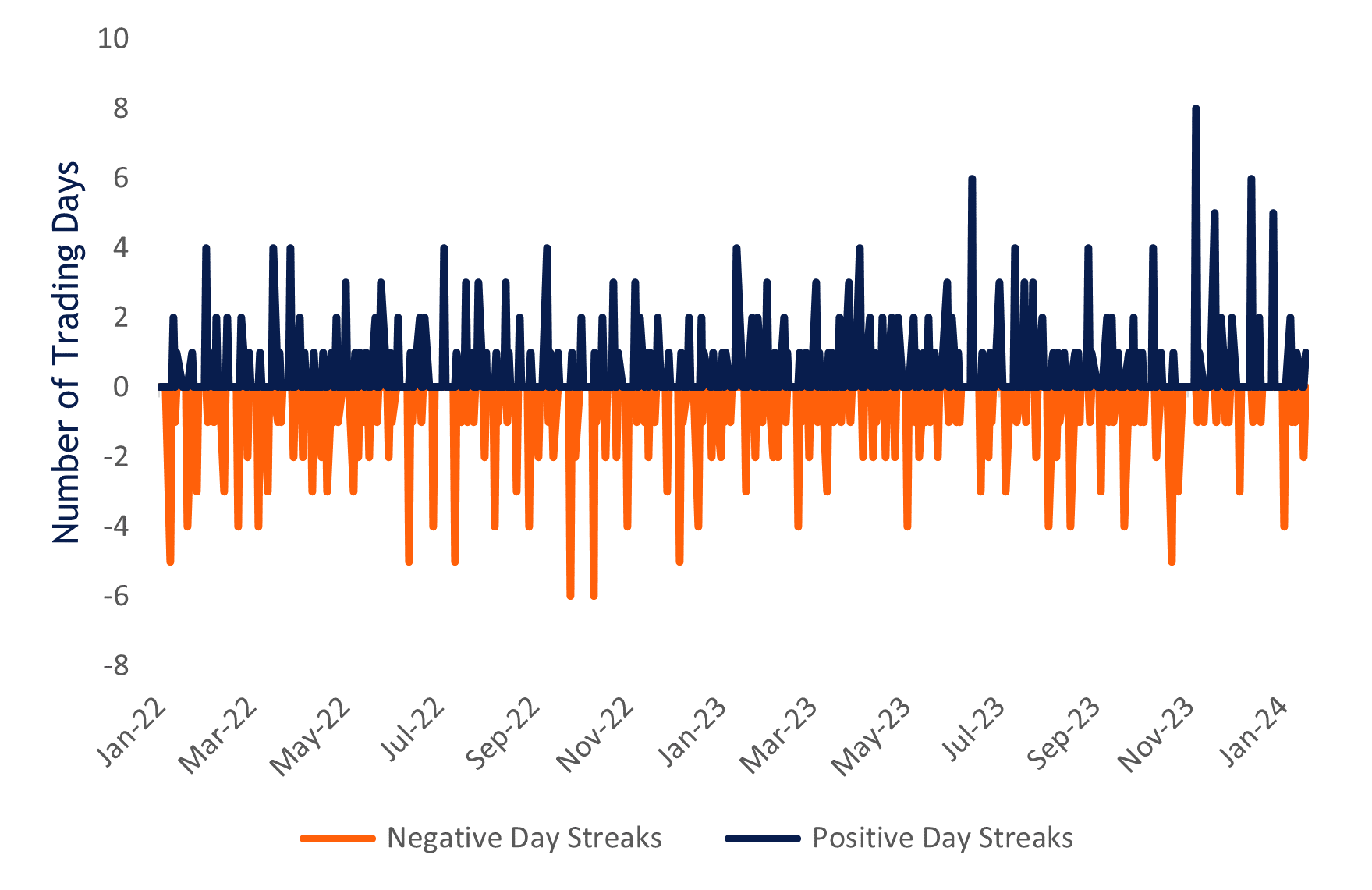

- Interest rate volatility (as per the MOVE index) remains elevated relative to the last decade but in line with the periods before central banks’ quantitative easing. We think interest rate volatility will remain elevated as long as the Federal Reserve (Fed) remains committed to reducing the size of its balance sheet. The most interest rate sensitive fixed income assets are likely at higher risk of volatility. But buy and hold investors should remember that bonds pay back principal at par regardless of intra-period volatility.

- After the recent back-up in yields, core fixed income sectors are trading close to levels last seen in early March and above longer-term averages. We think the risk/reward is more favorable for core bond sectors over plus sectors with the exception of the preferred securities market. As such, we think the recent move higher in yields is an attractive opportunity for investors to add to high quality fixed income.

IMPORTANT DISCLOSURES

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors. To determine which investment(s) may be appropriate for you, please consult your financial professional prior to investing.

Investing involves risks including possible loss of principal. No investment strategy or risk management technique can guarantee return or eliminate risk in all market environments. For more information on the risks associated with the strategies and product types discussed please visit https://lplresearch.com/Risks

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

Unless otherwise stated LPL Financial and the third party persons and firms mentioned are not affiliates of each other and make no representation with respect to each other. Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services.

All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

For a list of descriptions of the indexes and economic terms referenced in this publication, please visit our website at lplresearch.com/definitions.

Securities and advisory services offered through LPL Financial, a registered investment advisor and broker-dealer. Member FINRA/SIPC.

Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment advice from a separately registered independent investment advisor that is not an LPL affiliate, please note LPL makes no representation with respect to such entity.

- Not Insured by FDIC/NCUA or Any Other Government Agency

- Not Bank/Credit Union Guaranteed

- Not Bank/Credit Union Deposits or Obligations

- May Lose Value